Recently I’ve been thinking a lot about the direction I want to be headed financially, my sources of income, and how much money I need to make things happen.

I want to get into real estate investment and I have a lot of ideas about how I want to do this. Getting my credit repaired and my scores up will be a critical part of making this happen and it is one of the reasons I hit the ground running there. But there are obstacles remaining I have not yet tackled because I am still trying to figure out how. Last night, I tried to break things down and determine what was holding me back.

Even as my credit improves and I continue to build it up, there is one account that remains on my credit reports that, while reporting as current/paid as agreed, will no doubt hinder my ability to secure financing for real estate in the future. This is my account with Sallie Mae, my consolidated student loan account, currently reporting a balance of over $81,000. As I looked over this account in recent months, armed with the knowledge I have now, I am disgusted and ashamed of how irresponsibly I handled this account over the last seven years and it makes me ill thinking of just how much money it will ultimately have cost me.

Even as my credit improves and I continue to build it up, there is one account that remains on my credit reports that, while reporting as current/paid as agreed, will no doubt hinder my ability to secure financing for real estate in the future. This is my account with Sallie Mae, my consolidated student loan account, currently reporting a balance of over $81,000. As I looked over this account in recent months, armed with the knowledge I have now, I am disgusted and ashamed of how irresponsibly I handled this account over the last seven years and it makes me ill thinking of just how much money it will ultimately have cost me.

My original student loans totaled about $54,000 – at least that was the total balance after they had all been consolidated in 2007. The intended repayment term for most student loans is ten years – the interest rates are low, the payments spread out, and the average person would have them paid off by their early- to mid-thirties. If I had begun repaying my student loans in 2007 on a ten year plan:

Monthly Payment: $609.73

Total Principal: $54,000.00

Total Interest: $19,167.63

Paying an extra $100 each month would knock two years of payments off the loan and reduce the amount of interest I paid by over $4,000. That would have been one of the many options that would have been wise and prudent.

I instead let my loans remain in forbearance (and several times, my failure to remember the forbearance had ended allowed them to enter repayment, become delinquent, and put the negative payment history on my credit file I am dealing with today). Sitting in forbearance, the loan continued to accrue interest that was compounded (made part of the principal) and thus interest on the interest. The result: my student loan balance is now $30,000 greater but not because of more education.

I am scheduled to enter repayment next month – as my forbearance comes to an end. In order to pay this debt off in ten years, I would now be looking at the following:

Monthly Payment: $925.89

Total Principal: $83,000.00

Interest Paid: $29,106.00

And don’t forget that $30,000 of the principal IS ALSO INTEREST. The amount of interest I would be paying is greater than the principal balance.

If I can’t make that much of a payment and I instead pay according to the thirty-year repayment plan:

Monthly Payment: $511.57

Total Principal: $83,000.00

Interest Paid: $102,166.49

Monitoring my credit reports has also helped me see the magnitude of this situation as well. Each month that goes by, the amount owed on this account increases by over $400.00. Just to stop it from becoming even greater, I would need to pay over $400 per month!

This balance is comparable in size only to a mortgage – and that is how lenders will see it when I seek financing to buy real estate. This monthly obligation will affect the total expenses they will consider for me, since it is equal to a mortgage payment of its own.

There is no escaping this loan. It will never expire, never be dischargeable, never be settled. The only way to eliminate it, is pay it.

There is no escaping this loan. It will never expire, never be dischargeable, never be settled. The only way to eliminate it, is pay it.

I have to figure out how to tackle this loan. The best solution at this point is to pay it off as quickly as possible – doubling the monthly payment, for example, would pay the loan off in 4 years and would save me over $18,000 in interest paid. But that would be four years of monthly payments of $1,937, and at this point in my life, not even remotely possible. What I need is a large, lump-sum payment to immediately reduce the balance enough that the monthly interest being created is substantially reduced. This would make my monthly payments count for a lot more.

Figuring out how to do so is the trick.

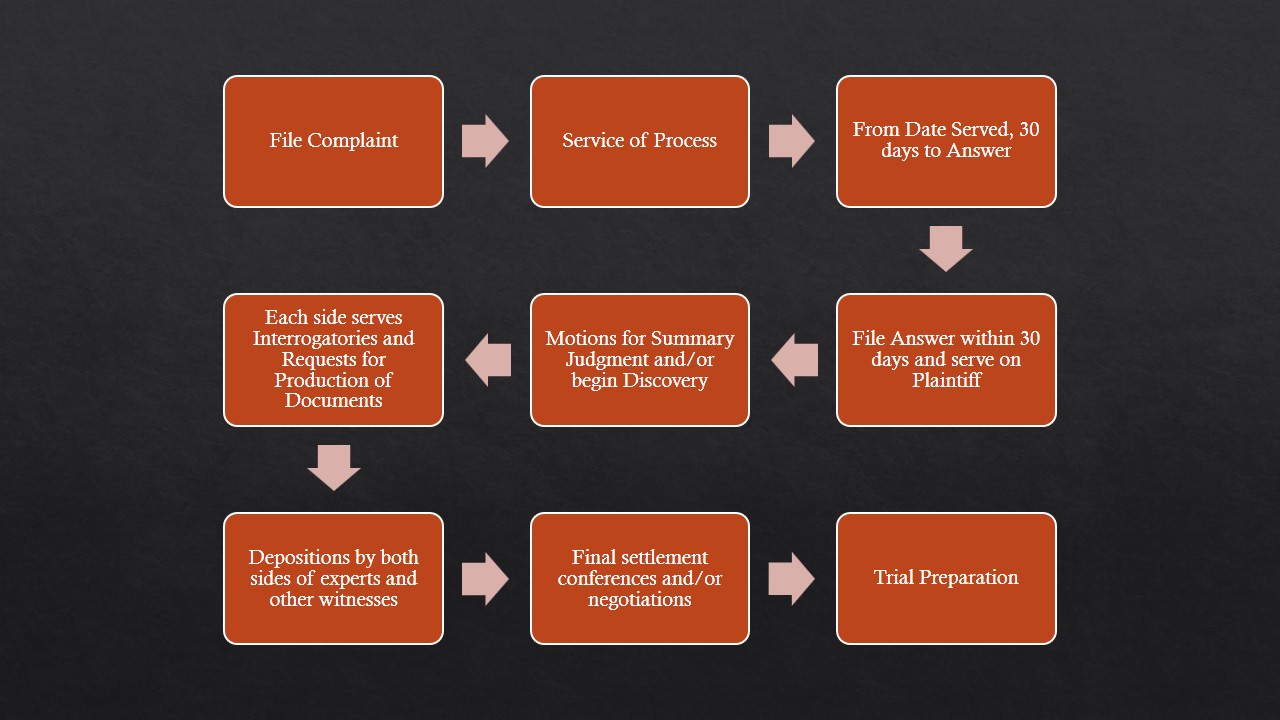

As I was about to drop the Complaint and Summons in the mail to the Sheriff for service, a light went off. NCS’ Registered Agent was listed as Joel Lackey, their CEO. NCS is headquartered in Atlanta, Georgia, presumably because that is where Lackey lives and he is the only owner of the company. You may be thinking, “and?” – but I was absolutely thrilled. Joel Lackey cannot be NCS’ Registered Agent in North Carolina – a company’s registered agent for a state has to live in that state.

As I was about to drop the Complaint and Summons in the mail to the Sheriff for service, a light went off. NCS’ Registered Agent was listed as Joel Lackey, their CEO. NCS is headquartered in Atlanta, Georgia, presumably because that is where Lackey lives and he is the only owner of the company. You may be thinking, “and?” – but I was absolutely thrilled. Joel Lackey cannot be NCS’ Registered Agent in North Carolina – a company’s registered agent for a state has to live in that state.